Financial real estate is in deep cyclical difficulties and has been forced to return to its main business! Real Estate: The "Land King" in the past

Cross Country Ski Strap is one of the new Hook And Loop products, those Winter Sports Ski Straps are with high-quality and imported raw materials manufacturing, environmental non-toxic. Our Custom Ski Strap favored by domestic and foreign sporting goods market in recent years. EVA Material Ski Straphas variety of colors, specifications to choose from, and colorful ski straps can print company LOGO as custom request.

Cross Country Ski Strap Cross Country Ski Strap,EVA Material Ski Straps, Winter Sports Ski Straps ,Custom Ski Strap Sunnice Reusable Pallet Wraps Co.,Ltd. , http://www.reusablepalletwraps.com

The three samples of the diversification of clothing companies, Youngor, Shanshan, and Red Bean, all need to calm down now.

According to last year’s financial report, Younger’s dual-industry structure with “real economy + virtual economyâ€, apart from achieving a modest growth in the basic industrial apparel segment, the real estate operating revenue that has been assigned to a performance-enhancing task has decreased by 46.94% over the same period, and the net profit of the financial investment sector. It was down by 60.90% over the same period. In contrast, Shanshan and Hongdou are also bad. Although the former increased 225% year-on-year in financial investment business, the lithium battery business invested heavily in the first time saw negative growth, a decrease of 8.31% year-on-year; and the real estate business of Hongdou even It was even worse than Youngor, which was down 48.42% year-on-year. Is it the time for the diversification of garment companies to re-deconstruct the moment?

In April of this year, Youngor’s chairman Li Rucheng stated in the quarter’s group economic work: “This year’s economic situation is grave, and company heads are ready to overcome the difficult times.†Youngor is facing the company’s most difficult period ever.

At the peak of Youngor's development, whether or not Li Rucheng admitted to replicating Buffett’s road, but in action, Youngor was indeed similar to Buffett’s Berkshire Hathaway: Originally, they were all textile and garment companies. Mainly financial investment. However, when Youngor almost created a truly Chinese version of Berkshire Hathaway, the dismal performance of 2011 made it return to the past.

What Li Rucheng is facing now is that companies are descending vertically from the peak to the bottom. What he has to do now is to try his best and do his best to change the speed of the "free fall," and seize effective time and space, and re-evaluate various industrial organizations. He proposed a solution: "Strictly control real estate investment, timely adjust the scale of investment, and concentrate resources on branded clothing." In other words, troikas that once led Youngor's real estate, financial investment, and apparel business are now required to make major Structural adjustments and returning attention again to the apparel business.

Then, on the return of the main garment industry, is Youngor a temporary emergency or a long-term strategic decision? This requires first asking, where are the real estate and financial investments? What is the driving force of the two heroes in the main business of returning to Younger?

The real estate business used to be Youngor’s strongest profit support. Before 2011, Youngor continued to increase its operating revenue in this business. In 2010, it reached a record high of 6.85 billion in revenue, however, with the decline of the real estate market. In 2011, Youngor's real estate business plummeted in 2011, causing Li Rucheng to drift away from the goal of “entering the top 20 domestic real estate in 2015â€. What is more important is that Youngor embarked on a dangerous capital steel.

Short-term liquidity tightened

According to the 2011 Youngor board report, the expected value of the real estate business this year has not been lowered: the pre-sales revenue will reach 5 billion, and the revenue will increase by more than 35%. “Is Younger’s real estate profitable and whether there is a real risk? It depends on the original cost of land acquisition, debt level, sales speed, and current property prices.†Gu Haibo, senior economist and independent economist at the Shanghai Changning Housing Development Bureau, told reporters In terms of short-term effects, the level of debt and sales speed are two core indicators to measure the risk of a real estate company.

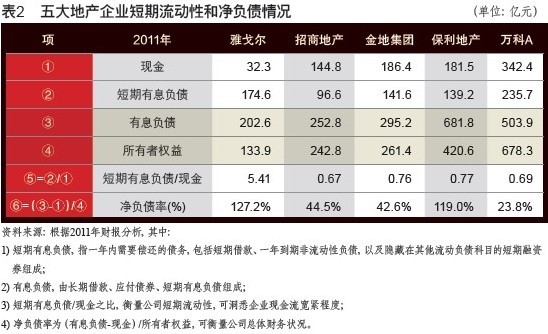

Let's look at Youngor's short-term debt level. Mainly based on two financial indicators: First, the proportion of short-term interest-bearing debt in cash, to measure its short-term liquidity; Second, the net debt ratio, measure its overall financial status. However, Youngor continued to suffer from poor performance on both indicators. Younger's 3.23 billion in cash, to deal with 174.6 billion short-term interest-bearing liabilities, the risk is self-evident, not to mention, according to earnings disclosure, there are 770 million in the cash is a "restricted currency funds."

Refinancing liabilities

If you do not have enough cash, you need to speed up the sale of real estate. However, real estate income dropped from 6.85 billion in 2010 to 3.64 billion in 2011. It is also enough to confirm that the real estate regulation has a huge impact on Youngor's real estate business, making it difficult to sell its houses.

According to the financial report, taking Xixi Qingxue, a project that has not yet been completed but is being pre-sold in 2011 as an example (see Table 3), 9.83% has been pre-sold at the end of 2010, and the proportion of pre-sales at the end of 2011 is 15.38%. The equivalent of only selling 5.55% in 2011. Assuming that the control policy is not too tight, according to this rate, the property will take a total of 15.25 years to sell out, which means that the entire project will be sold for another 14.50 years even after it is completed in September 2012. What is even more severe is that, due to the downturn in the property market, there have been two discount promotions. According to the survey, the first round of discounts was calculated in the third quarter of last year, according to a discount of 7.44 yuan from the opening price of 30,000 yuan per square meter, which was 22,320 yuan per square meter. The second round of discounts was lowered again on April 27 of this year. To 22,000 yuan / square meter, indicating that the real estate sales situation is worrying.

Zhang Jiaxi, director of marketing of Suzhou Youngor Real Estate Co., Ltd., which is responsible for the Jiangsu market, said that “the real estate control is like a flag. It is not known that after the chess is full, the board is limited, and finally everyone is suffocated.†Houses are difficult to sell, and subject to the impact of real estate regulation, Youngor must also reflect on his own problems.

In the same way as Li Rucheng used “radical strategy†in the past and gave a big push in the real estate market, he now fell to Greentown holding boss Song Weiping who was rescued by the Wharf Group in Hong Kong. He recently introspected himself: “No disaster was predicted (regulation of The length and depth of the blow) I need to review." Perhaps, Li Rucheng's understanding of this sentence is more profound than the average person.

Youngor on the capital wire

The three samples of the diversification of clothing companies, Youngor, Shanshan, and Red Bean, all need to calm down now.