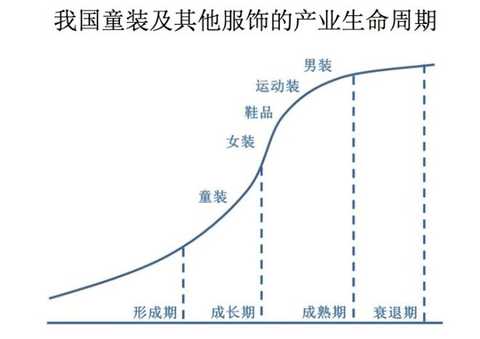

On June 1, Shenzhen Annaier Co., Ltd. (hereinafter referred to as “Annelâ€) officially landed on the Shenzhen Stock Exchange with the stock code 002875. The stock was also regarded by the industry as “the first share of A-share children's wearâ€, and was temporarily suspended by the exchange due to a 44% increase after the opening. The An Nai IPO issue price is 17.07 yuan per share, and the net proceeds are 379 million yuan, mainly used for marketing center construction projects, design and development center construction projects and information construction projects. "Annil Ann's" was formerly known as "Annier Children's Clothing Store." The brand has been in business for more than 20 years since its establishment in 1996. It is a private label clothing enterprise specializing in high-end children's wear business. Engaged in the core business links of independent research and development design, supply chain management, brand operation promotion and direct sales and franchise sales in the value chain of children's wear products. And the company's products cover two major categories of children's wear and children's wear, including tops, coats, pants, skirts, down jackets, home clothes and many other categories. Its business model is also a combination of online and offline modes. The e-commerce channel mainly cooperates with many well-known domestic e-commerce platforms such as Taobao, Tmall, Vipshop, and Jingdong. In 2016, the proportion of e-commerce business revenue has reached 24.32%. The offline is mainly direct sales, mainly in first- and second-tier cities. As of the end of 2016, Anna has a total of 1,458 stores, including 970 directly operated stores. China's children's wear market has a large room for growth According to the "Infant and Child Industry Special Report - Investment Future, Sharing Growth" published by CITIC Securities Research Institute, on the one hand, China's children's wear is still in the growth stage, compared with mature women's wear, shoes, sportswear and men's wear. There is still a large room for growth. On the other hand, compared with some developed countries, the per capita consumption of children's wear in China in 2013 was only 13.8 US dollars, far lower than the market consumption of Japan's 66.3 US dollars, the US's 90.7 US dollars and the United Kingdom 137.2 US dollars. At the same time, the market share of the top ten Chinese children's wear has also increased from 5% in 2008 to 12.5% ​​in 2016, but there is still a big gap compared to 40.4% in the US. Industry life cycle picture of Chinese children's wear and other apparel Under the influence of the comprehensive liberalization of the "two children" policy and the upgrading of consumption, China's children's wear market is ushered in a period of rapid development. After all, due to the high frequency of children's clothing updates, there is a rigid demand in household consumption. In addition, most of the young parents who have entered the peak of childbirth are the only children born after the 1980s. They are generally well-educated, have higher requirements for quality of life, and pay more attention to the concept of parenting for prenatal and postnatal care. At the same time, after a long-term increase in income level, the consumption expenditure of modern family children has been based on the accumulation of wealth of two generations, which has amplified and promoted the realization of the consumption demand of baby products. It is estimated that by 2018, the size of the children's wear market is expected to reach 194.1 billion yuan, and this figure was only about 116.4 billion yuan in 2013. In 2010-2016, China's children's wear market maintained a compound annual growth rate of 9.5%, which is the most stable sub-sector in the apparel industry. Industry competition is intensifying, Barabara is no longer a big one As mentioned above, China's children's wear started late, the market concentration is low, and the R&D and production levels of various enterprises are uneven, which further restricts the development of the children's wear industry. According to the statistics of the China Business Federation, in 2015, the national top ten brands in the national large-scale retail enterprises had a total market share of 25.23%. Among them, Senma's children's wear Parabala topped the list with a market share of 3.91%. 2015 children's wear TOP10 market comprehensive share picture In fact, revenue has been growing steadily since Senma established the “Balaba†children's brand that positioned the middle class and the well-off home in 2002. Looking at its earnings report from 2012 to the present, the income of children's business accounted for 29.94%, 34.75%, 38.87%, 41.81%, and 46.88%, respectively. For this reason, Barabara is also known as "the first brand of Chinese children's wear." However, with the strong presence of some foreign brands, and the rise of more and more children's wear brands in China, the status of their children's wear boss has also been shaken. From the top 10 companies in the market with a market share of 2015, it is also obvious that Adidas, which ranks second, is only 0.04 percentage points lower than that, and Ann Arbor, which just listed, ranks 4th with a market share of 3.34%. . Just in March 2017, Carter's, the largest baby and baby wear brand in the United States, also announced its formal entry into the Chinese market, and the competition will become increasingly fierce. Children's wear competitor details picture At the same time, there have been a number of brands that extend from adult wear to children's wear. The same is true of Adidas mentioned above, which is the same reason that Senma extends from casual wear to children's wear Barabara. In addition to some of the brands mentioned above, there are also domestic children's wear brands such as Taiping Bird, Jiangnan Cloth, Xtep, and 361 Degrees; foreign countries like ZARA, H&M, GAP, Uniqlo, etc., which also have their own children's wear. line. Their children's wear usually maintains a similar design style to their adult wear, using the original brand advantages and channel resources to promote children's wear products. For example, adding a children's wear area or shelf in an existing retail terminal channel to form a comprehensive store model. Domestic and foreign children's clothing analysis pictures The lower gross profit margin may also become the main culprit for Barabara's lack of stamina and “retreating to the second lineâ€. It is reported that Barbara's gross profit margin from 2014 to 2016 was 42.01%, 41.09% and 42.87% respectively. Below the industry average of 53.79%, 51.51% and 52.08%. Industry operating gross profit margin comparison chart In fact, in addition to the above, China's children's wear industry still has a certain gap compared with the international advanced level in terms of fabric research and development, functional design and style design. To truly open the market, it has strong competitiveness. On the basis of good products, it is also crucial in brand operation and user interaction. Nantong NATASHA Textiles Co.,Ltd. , http://www.ntnatashatextile.com